- Services

- Sectors we serveAsset Managers

Unlock the full potential of your portfolio with Adepa’s tailored solutions. From regulatory compliance to operational efficiency, discover how we empower asset managers to achieve strategic growth and navigate the complexities of today’s financial landscape.

Wealth ManagementExplore Adepa’s Wealth Management services, designed to enhance operational efficiency, ensure compliance, and deliver personalized strategies. Discover how we can support your success in a competitive financial landscape.

Private MarketsAdepa offers tailored solutions to address the complexities of Private Markets. From fund structuring to regulatory compliance, our expertise helps you manage risks, enhance operational efficiency, and achieve long-term success in a competitive financial environment.

CorporationsAdepa provides essential corporate services that streamline operations, ensure regulatory compliance, and support strategic growth. Explore how our solutions can help your corporation thrive in a competitive landscape.

- About UsOverview

Discover Adepa’s strong foundation and global reach, providing personalized financial solutions across various industries.

Our PeopleMeet the dedicated professionals driving our commitment to excellence and innovation in the financial services industry.

CareersPursue fulfilling careers at Adepa and unlock new opportunities for professional growth and success.

HistoryExplore Adepa’s history and key milestones, from its foundation to global expansion, highlighting significant achievements in the financial services industry.

- BlogBlogExplore expert insights and updates on industry trends, regulations, and best practices through our latest blog articles.

- NewsNews

Adepa successfully completes acquisition of Fidupar

October 2, 2024March 24, 2022Adepa & Cesam: Joint support for the group Azimut

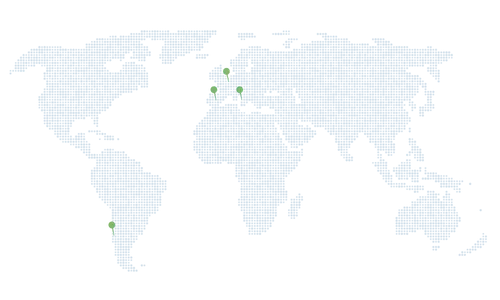

February 16, 2022 - Contact UsAdepa in the world

Discover Adepa’s global presence. Our offices span key financial hubs, ensuring close partnerships and tailored services across various regions.

Contact UsGet in touch with Adepa for personalized assistance. Whether you have questions or need support, our team is ready to assist you with expert guidance.

NewsletterStay updated with Adepa’s latest insights and news. Subscribe to our newsletter and be the first to receive updates on industry trends, services, and company developments.